yahoo Press

A Look At BYD's (SEHK:1211) Valuation After 2025 Profit Drop And Dividend Cut

Images

1 / 4

2 / 4

3 / 4

4 / 4

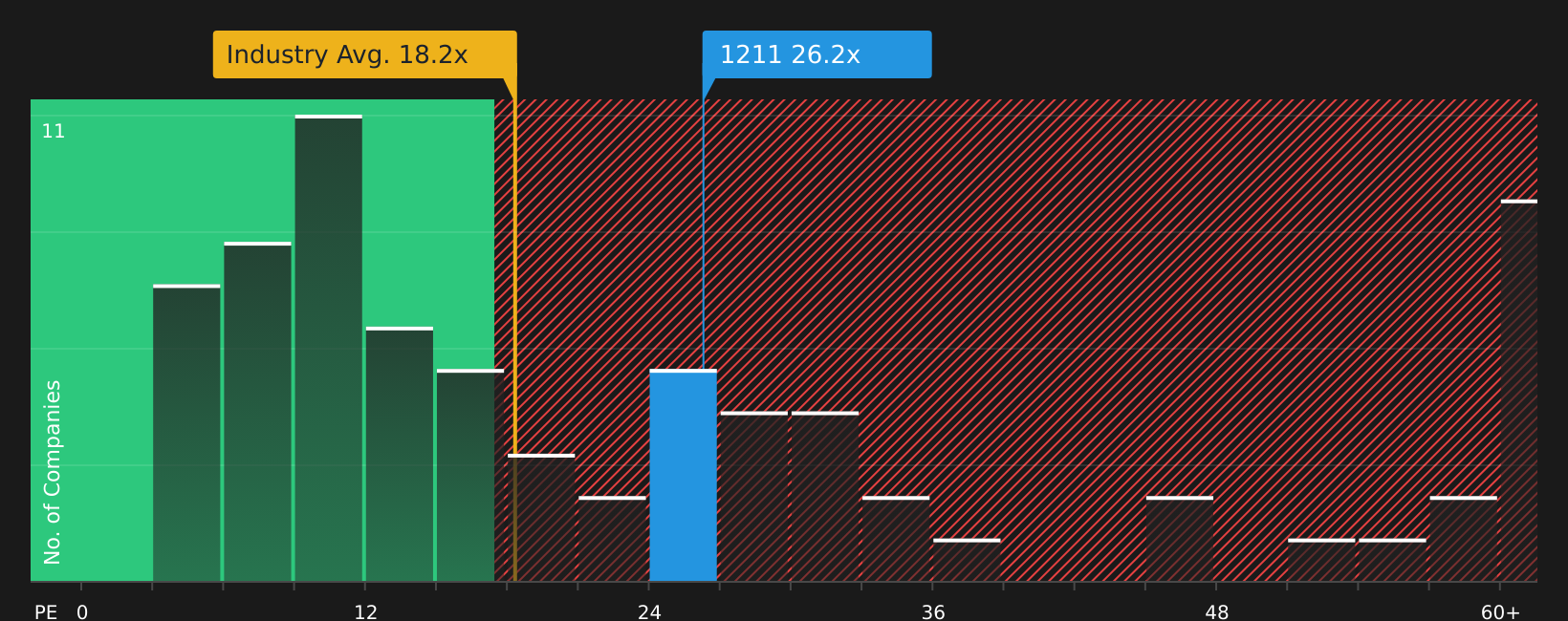

Find your next quality investment with Simply Wall St's easy and powerful screener, trusted by over 7 million individual investors worldwide. BYD (SEHK:1211) has delivered higher full year 2025 sales of CNY 803.96b, but net income is down to CNY 32.62b, alongside a lower proposed final dividend of RMB 0.358 per share. See our latest analysis for BYD. BYD’s latest earnings setback and lower proposed dividend come after a period where the share price has picked up, with a 30 day share price return of 12.16% and a 90 day share price return of 13.78%. However, the 1 year total shareholder return is still down 20.59%, while the 3 year and 5 year total shareholder returns of 43.41% and 85.91% indicate that longer term investors have seen much stronger gains. This suggests that recent momentum is rebuilding after a tougher year. If you are reassessing BYD after these results, it can help to compare the stock with other electric vehicle and battery related names by checking a curated list of 26 best rare earth metal stocks With the share price still down 20.59% over 1 year, trading at an estimated 45% discount to one intrinsic value estimate and below the average analyst price target, is there a genuine opportunity here, or is the market already pricing in future growth? BYD’s latest narrative fair value of HK$180.00 stands well above the last close of HK$106.50, which raises clear questions about what is built into that gap. Company over priced against my share purchase entry point. Likely, due to over excitement on EV's versus practical realities regarding charging infrastructure support and full understanding of environmental impacts (carbon footprint) Read the complete narrative. Read the complete narrative. Want to see what justifies that higher fair value? The narrative leans heavily on long term revenue expansion, healthier margins, and a future earnings multiple that assumes sustained demand. Curious which expectations matter most to that HK$180.00 figure and how they stack up against today’s 1 year share price decline and recent earnings softness? The full narrative joins those numbers into a single valuation story that you can test against your own view. Result: Fair Value of HK$180.00 (UNDERVALUED) Have a read of the narrative in full and understand what's behind the forecasts. However, this narrative could be shaken if tariffs on Chinese EVs tighten further or if buyers instead shift meaningfully toward hybrids and alternative fuels. Find out about the key risks to this BYD narrative. The narrative fair value points to BYD looking undervalued, but the P/E ratio tells a tighter story. At 26.2x earnings versus 18.2x for the Asian auto industry and a fair ratio of 15.8x, the shares carry a clear valuation premium that could compress if sentiment cools. That gap between the current P/E of 26.2x and the fair ratio of 15.8x highlights real pricing risk if the market eventually settles closer to the level suggested by the regression. How much of that premium are you comfortable paying for the BYD story? See what the numbers say about this price — find out in our valuation breakdown. Mixed signals can make any stock feel harder to judge. If this update leaves you on the fence, take a closer look at the data and decide quickly where you stand, then weigh the 2 key rewards and 1 important warning sign. If BYD’s mix of growth potential and valuation questions has your attention, do not stop here. Use these targeted stock ideas to pressure test your portfolio. Spot fresh potential by checking companies that screens highlight as screener containing 599 high quality undiscovered gems before they appear on more radar screens. Strengthen your core holdings by reviewing financially sound names surfaced in the solid balance sheet and fundamentals stocks screener (383 results) so weak balance sheets do not catch you off guard. Lean toward resilience by scanning for companies with steadier profiles in the 270 resilient stocks with low risk scores while others focus only on headline stories. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Companies discussed in this article include 1211.HK. Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com